February 27, 2025 News:

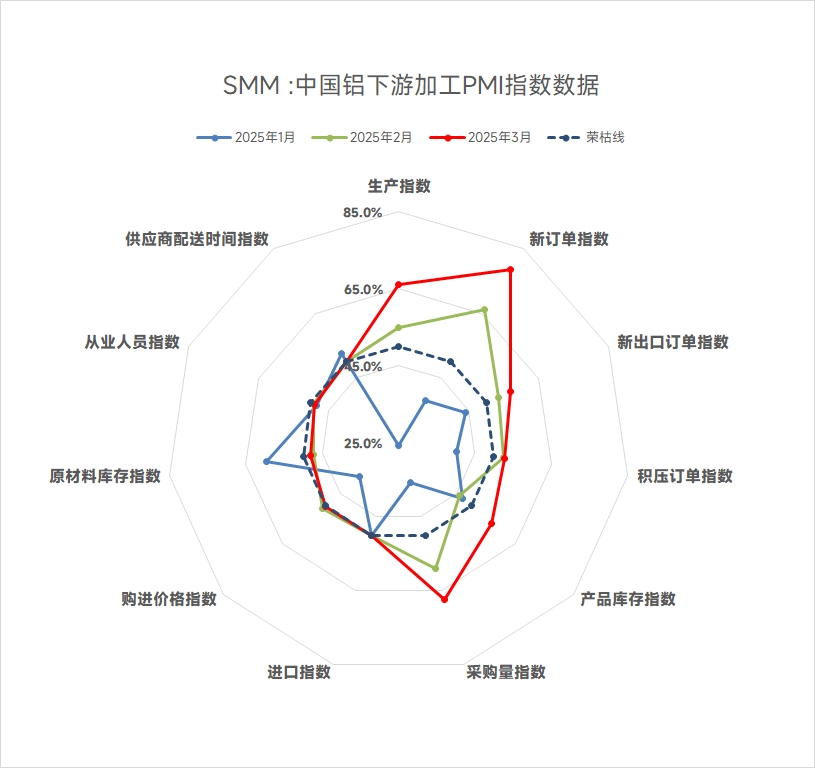

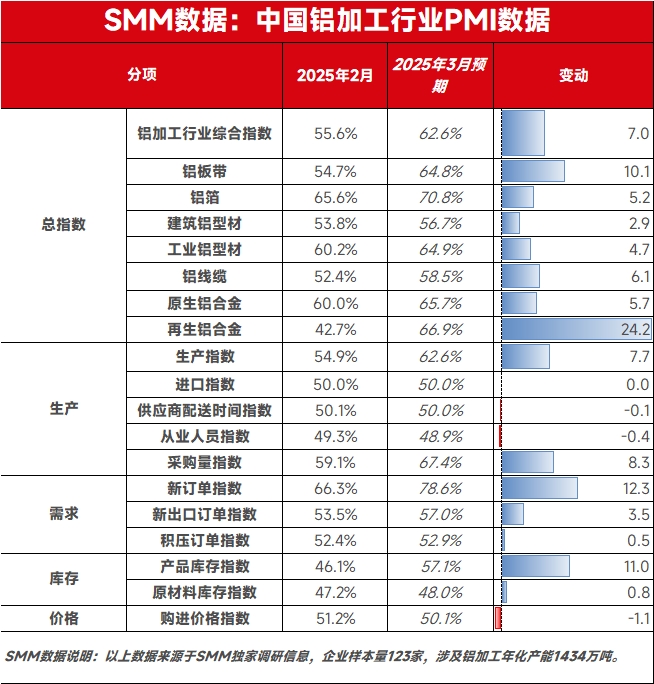

According to SMM data, the composite PMI index of China's aluminum processing industry recorded 55.6% in February 2025, remaining above the 50 mark.

By product type:

Aluminum Plate/Sheet and Strip: The PMI for the aluminum plate/sheet and strip industry in February was 54.8%, up 17.6 points MoM. Although the market gradually resumed trading after the Chinese New Year holiday in early February, inquiries and orders fell short of expectations. This was mainly due to sufficient stockpiling by downstream end-users before the holiday, resulting in low restocking willingness. By product, high-value-added products such as automotive and aerospace plates were less affected by the holiday, with relatively stable orders, while demand for other products still awaited recovery. By late February, the benefits of multiple economic stimulus policies introduced by the government gradually extended to the aluminum plate/sheet and strip sector, leading to increased orders from downstream customers of some enterprises. With the arrival of the traditional consumption peak season, demand for automotive and battery-related products rebounded significantly. The PMI for the aluminum plate/sheet and strip industry is expected to continue its upward trend in March.

Aluminum Foil: The PMI for the aluminum foil industry in February recorded 65.6%, significantly rising above the 50 mark. After the Chinese New Year holiday, most downstream customers of aluminum foil plants resumed production, leading to a gradual increase in orders for aluminum foil enterprises. By product, the seasonal air-conditioner foil saw optimistic order recovery due to the approaching peak season and government subsidies stimulating the home appliance consumer market. Orders for battery foil also showed significant YoY growth, while other aluminum foil products, such as packaging foil, remained relatively stable. Entering March, the traditional peak season, leading aluminum foil enterprises are expected to see further order growth. However, the overall market remains in oversupply, and cut-throat competition in the industry may limit further increases in the PMI index.

Construction Aluminum Extrusion: The composite PMI index for the construction aluminum extrusion industry in February recorded 53.75%, rebounding above the 50 mark. According to the SMM survey, most of the industry resumed production after the Lantern Festival, with production levels remaining flat compared to the previous month. The production index rebounded to 46.51%. On the raw material side, aluminum prices remained high in February, and only small-scale stockpiling was conducted for safety inventory. The raw material procurement index for the month recorded 52.13%, while the inventory index stood at 42.26%. Additionally, with ongoing tenders in various regions, new orders for related enterprises increased, with the new orders index recording 68.63%. Domestic orders remained the primary focus for the construction aluminum extrusion industry. Although tariff policies impacted exports, related export enterprises renegotiated overseas orders, resulting in some spot order exports. The export orders index rebounded to 60.1%. Entering March, the traditional peak season for construction aluminum extrusion is expected to drive the PMI index higher.

Industrial Aluminum Extrusion: The PMI for the industrial aluminum extrusion industry in February recorded 60.22%, significantly rising above the 50 mark. By sub-index, the production index recorded 51.22%, and the new orders index reached 83.88%, mainly driven by the gradual recovery of industrial extrusion production in February, especially the surge in orders for automotive extrusion and the resilient demand in the PV sector. Consequently, the raw material procurement volume index for processing enterprises remained above the 50 mark, recording 66.58%. Additionally, according to the SMM survey, despite high aluminum prices, processing fees declined, and intense competition in the industry led to widespread pressure to reduce inventory and costs. Most manufacturers adopted production strategies based on order volumes, maintaining only safety inventory, which caused the raw material inventory index to drop to 41.41%. Meanwhile, as products are primarily customized, finished product inventories were mainly used for shipment turnover, with the finished product inventory index slightly rising to 53.59%. The rapid recovery in the automotive sector and stable demand in the PV sector have led the industry to hold an optimistic outlook for aluminum extrusion demand in March, with the PMI for the industrial extrusion sector expected to remain above the 50 mark.

Aluminum Wire and Cable: The composite PMI index for the domestic aluminum wire and cable industry in February recorded 52.4%, driven by steady post-holiday resumption of work and accelerated order fulfillment, keeping the PMI above the 50 mark. Aluminum wire and cable enterprises resumed normal operations after the Lantern Festival, but due to relatively relaxed order delivery cycles, post-holiday production did not fully recover, remaining sluggish. The production index for February recorded 47.15%. Regarding new orders, the accelerated fulfillment of ultra-high voltage transmission and transformation orders after the holiday drove the new orders index to 57%, with the industry maintaining an optimistic outlook. Post-holiday restocking demand and the landing of new orders led to increased procurement volumes, with the procurement index recording 63.60%. Anticipating subsequent deliveries, finished product inventories also increased, with the related index recording 60.48%. Entering the traditional consumption peak season of March and April, aluminum wire and cable enterprises are expected to maintain stable operations. However, as the power grid delivery cycle has not yet arrived, a full rebound in production is unlikely. The PMI for the aluminum wire and cable industry is expected to remain above the 50 mark in March 2025.

Primary Aluminum Alloy: The PMI for the primary aluminum alloy industry in February was 60.0%, up 12.8 points MoM. The first half of February remained an off-season for the primary aluminum alloy sector, with some producers adopting a wait-and-see approach and maintaining a slow production pace. In the second half of February, as downstream sectors resumed post-holiday operations after the Lantern Festival, demand improved, and the operating rate of primary aluminum alloy gradually returned to pre-holiday levels. Currently, the primary aluminum alloy market is in a "weak recovery during the off-season" phase. During the transition from off-season to peak season, demand recovery has been slow and uneven. Some enterprises increased production due to improved orders, while others reported demand lagging behind supply, focusing on digesting in-plant inventory. The industry as a whole awaits the arrival of the peak season (after March) to confirm substantial improvement. Enterprises need to balance inventory control with flexible production adjustments. SMM expects the PMI for the primary aluminum alloy industry to have further room for improvement in March.

Secondary Alloy: The PMI for the secondary aluminum industry in February rebounded 14.6 points MoM to 42.7%, but it remained below the 50 mark. Production was significantly impacted by the Chinese New Year holiday, with most secondary aluminum plants shutting down furnaces and taking holidays in early February. Post-holiday resumption was slow, and the fewer working days in February led to a general decline in production. Additionally, delayed resumption by aluminum scrap traders resulted in reduced aluminum scrap procurement and raw material inventory for secondary aluminum plants. On the demand side, downstream enterprises had low operating rates in the first one to two weeks after the holiday. Coupled with persistently high aluminum prices, die-casting enterprises primarily focused on digesting pre-holiday inventory, leading to sluggish market transactions. By mid-February, market demand recovery remained slow, and new orders for enterprises decreased. Looking ahead to March, as downstream demand gradually normalizes, market consumption expectations are improving, and the PMI for the industry is expected to rebound above the 50 mark.

Brief Analysis:

In February, aluminum prices continued to rise, driven by strong macro sentiment after the holiday. SHFE aluminum showed robust upward momentum, breaking through the 21,000 yuan mark and maintaining a high-level consolidation, poised for further gains. On the fundamentals side, most downstream sectors of aluminum processing resumed operations as expected after the holiday. The landing of new orders helped processing enterprises improve production efficiency and purchasing pace, with the industrial extrusion sector performing particularly well. The new energy sector continued to drive incremental consumption of aluminum. Considering the arrival of the traditional consumption peak season in March and April, as well as market expectations for the Two Sessions, March is likely to see continued growth in industry orders and improved production efficiency among downstream manufacturers. SMM expects the PMI for China's aluminum processing industry to remain above the 50 mark in March.

》Click to view the SMM Aluminum Industry Chain Database

(SMM Aluminum Team)